Boris Johnson, the new British Prime Minister promised the “beginning of a new golden age” in his inaugural speech. Sounds like Britain has a dose of Trump coming its way. As per the Oxford Dictionary, Golden Age is defined as “an idyllic, often imaginary past time of peace, prosperity, and happiness.” The one part that I can see happening is the “imaginary” part. Here is why

BJ promised to renegotiate Brexit while EU leaders immediately clarified there won’t berenegotiations especially about issues Johnson promised to renegotiate (among other things the “Irish Backstop“).

All this does not sound like the coming of a golden age, actually, it sounds like the opposite. But if BJ can say it at least three times it may come true or at least people may think it becomes true according to “Trump’s Rule” which he called “truthful hyperbole” as he laid out how he enjoys “playing with people’s fantasies.”

Brown and Irwin have a wonderful piece documenting the importance of US tariffs as a source of government revenue. The two economists parse Trump’s recently tweet:

“Billions of Dollars are pouring into the coffers of the U.S.A. because of the Tariffs being charged to China, and there is a long way to go. If companies don’t want to pay Tariffs, build in the U.S.A. Otherwise, lets just make our Country richer than ever before!”

Here is what they find

1. The United States gets 98 percent of government revenue from non-tariff sources.

2. Raising revenue through tariffs is more costly than other forms of taxation.

3.Raising revenue from tariffs generates fairness concerns.

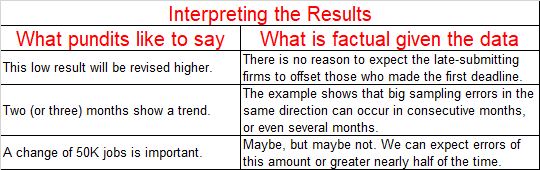

The monthly release of the US Payroll data is always a key indicator of economic activity. Jeff Miller parses what we should and should not read into the payroll data. Here is the abstract:

A) Job creation and destruction exceeds 2 million per month, so the neteffect is likely going to be relatively small – despite the fact that the economy created millions of jobs.

B) The reported payroll data is the changein the net, reducing the magnitude of the payroll data even further.

C) But most importantly, the payroll data ist is not the actual change in payroll jobs based on a surveyed sampleof US businesses.

D) Given the size of the US workforce (~150 million), the sampling error implies a 90% confidence interval of 112,000 jobs! This means that if 100 samples were taken, the mean of 90 of the 100 samples would contain the true mean, but that these 90 samples could differ up to 112,000 jobs.

This has important implications for the interpretation of payroll results:

Below the analysis from Brad Setser, who is known for his meticulous knowledge and analysis of international data. Here is what the reform promised:

“Trillions of dollars in trapped profits will return to the United States… We expect that it could be — the number started out at about $2.5 trillion; we think it’s going to be close to $5 trillion,” he [Trump] said, speaking to business leaders. “Over $4 [trillion], but close to $5 trillion, will be brought back into our country. This is money that would never, ever be seen again by the workers and the people of our country.” (Source)

But wait, there were more bombastic promises: “With a lower tax rate, U.S. firms will no longer have an incentive to offshore” said Kevin Hassett (Trump’s Chair of the Council of Economic Advisors): “There is also a literature that looks at the relationship between tax rates and transfer pricing. That literature implies that a corporate tax cut to 20 percent would dramatically reduce the trade deficit and increase GDP accordingly.”

And finally, The Trump White House: “The tax cuts will make America a more competitive location for manufacturing.” “American manufacturers are optimistic like never before, because President Trump’s tax cuts and relief make them more competitive.”

All three arguments come up short when compared to the data. It is not true, as Setser shows that “With the tax reform, there is no longer a tax incentive to maintain the whole “offshore” profit charade… What has happened? Some money has moved back (as one would expect), but not all that much and as of the first quarter [of 2019] firms returned to “reinvesting” a portion of their offshore profit back abroad. The cumulative sum of “reinvested earnings” is rising again.”

Given all the rhetoric about the cost to the United States of all these trapped profits, the reality that only a small amount, on net, has come back to the United States should be a bit sobering. It turns out that most firms weren’t all that inconvenienced by their large offshore cash balances. Those that really wanted to do a buyback could borrow against their offshore profits. Those that wanted to wait until the tax code changed before doing a buyback could do that too, as the market expected that the bulk of the cash would eventually be returned to shareholders.

Technically speaking, about $248 billion of formerly offshore profit was returned (That is the sum of the “negative” numbers on reinvested earnings, and sum consistent with the findings of the Wall Street Journal, which found a roughly $300 billion drop in the overall cash balance of U.S. firms in 2019)… Substantively, what really matters is whether the new tax code got rid of the incentive for firms to “offshore” a large portion of their profits. And the answer is clear. It didn’t.

The amount of profit that American firms report in the world’s low tax jurisdictions is the strongest single bit of evidence that the current process of globalization needs to be reformed. U.S. firms report to earn about 1.5 pp of U.S. GDP in Ireland, the Netherlands, Switzerland, Singapore, and a bunch of really small Caribbean islands. That is far more income than U.S. firms report in large market countries like Germany, France, Italy, China, Japan, India, and Mexico. Clearly something is going on (the countries in Europe are well aware of this, the non-taxation of the profits U.S. tech firms earn in Europe has long vexed them).

The data on the global distribution of U.S. FDI tells the same story—the majority of FDI by value is now claims on those same low tax jurisdictions (Don’t trust me? Look at table 1 of the BEA’s release on U.S. direct investment abroad and the IRS data on what kind of profits U.S. firms report and what kind of tax they pay in different jurisdictions). What happened after tax reform? The profit U.S. firms report in these low tax jurisdictions went up.

A new Fed paper outlines the “local content” in US Imports, to highlight that trade is not “us against them” but that global supply chains are intertwined. It is well known that Apple designs in the US, builds components globally, and assembles its phones in China. That is one reason why US tariffs on Chinese goods hurt not only China, other countries that produce intermediate inputs, and also the US itself!

“When you buy a $100 pair of Nike sneakers made in Asia, only $25 of its cost goes to the Asian factory that assembles the shoes (Kish 2014). Of the remaining $75, $3.50 is spent on shipping from Asia to the United States, and $21.50 goes to Nike to cover its design, marketing, profits, and other expenses. The remaining $50 goes to the U.S. retailer that pays for the transportation of the sneakers inside the United States, worker wages in its U.S. warehouses and retail outlets, rental cost of retail space, insurance, and so on. Thus, half the cost of a pair of sneakers made abroad pays for workers and capital expenditures in the United States, not even counting the part that goes to Nike.

When you buy a MADE IN THE US of A Jeep Patriot, manufactured in Illinois, at least 17% of the cost goes to parts made in other countries (NHTSA 2017). Thus, even for a car that is manufactured in the United States, a substantial part of its cost traces to imported intermediate parts used in its production.

These examples are useful to understand how raw statistics on imports fail to fully account for the cost of imports, and how part of the cost of American goods and services reflects imports. The Fed study accounts for the US (“local”) content of US imports and finds that for some countries (including China) over half of the expenditures for imports flows back to US companies and workers.”

In May 2019, President Trump declared a national emergency regarding potential threats posed by foreign technology companies and blacklisted the Chinese Company Huwwei to prevent it from conducting business with U.S. companies. The U.S. Department of Justice (DOJ) had charged Huawei in January 2018 with bank fraud and stealing trade secrets as well as crimes including conspiracy, money laundering, bank and wire fraud, flouting U.S. sanctions on Iran, and obstruction of justice.

Several dozen(!) countries intoduced bans on Huawei, followed the US lead on Huawei either because they were strong-armed or because they trusted the US threat assessment.

Six weeks later, Trump declared Huawei open for business again and all other countries that shut down Huawei for supposed national security reasons now sit with egg on their faces. Even Republican senators noted that no one will believe the US anymore if one day it declares a country/company a threat to national security and on the next day declares it open for business.

“Trump on Monday [7/1/2-19] said talks have already begun. “They’re speaking very much on the phone and also meeting,” he told reporters at the White House. A spokesperson for [US Trade Representative] Lighthizer said there no scheduling announcements at this time. “The date is not set. The city is not set,” said one person close to the talks, when asked by Morning Trade about when U.S. Trade Representative Robert Lighthizer might sit down with Chinese Vice Premier Liu He.”

We also learned some interesting new pieces if information about these negotiations. They are no longer about tariff reductions but about changes in laws. The “U.S. still wants China to change its laws to implement commitments to combat forced technology transfers and other intellectual property transgressions.” “China wants the U.S. to also amend its laws that Beijing views as hostile to Chinese companies.” You be the judge how likely any of these outcomes are…

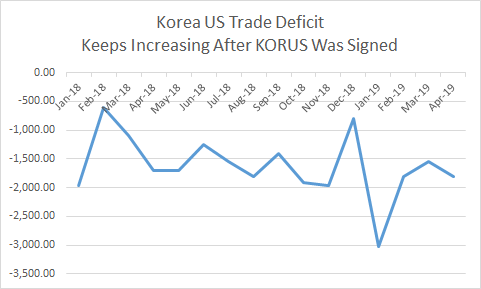

After the G20 summit in Japan, US President Trump went to the only country where he could claim a sealed trade agreement: South Korea (Trump signed a slight update of the comprehensive 2012 Korean-US trade agreement). In Korea he toasted the deal as evidence he’s winning.

But in Washington officials were confronting a grim new reality for U.S. economic power. When Trump dialed up the heat with tariffs and threats, the rest of the world looked elsewhere for opportunities: Bloomberg reports that the European Union is taking advantage of the void created by Trump’s lack of Free Trade leadership by signing historic trade deals with Japan, Latin America, and Vietnam benefiting EU firms in these key markets over US firms.

“For two decades, Europe had been trying to nail down a pact with Brazil, Argentina and the two other members of Mercosur, a bloc traditionally known for its nationalist approach to industrial policy and protectionism. But hours before Trump and Xi met, the EU announced the deal was finally done. The message was stark. European industrial giants such as Airbus and Siemens would gain an advantage over their U.S. competitors in Latin America. Argentinian and Brazilian farmers would win an edge in Europe over U.S. competitors, adding to the decline of America as an agricultural export power… With Trump threatening the global order, officials in Brussels, Brasilia and Buenos Aires had spied an opportunity to forge the new economic alliance — just as the EU and Japan had in a deal that took effect earlier in 2019. A day after the leaders left Osaka summit, the EU signed a deal with Vietnam, a nation Trump just days earlier lambasted as ‘almost the single worst abuser of everybody.’”

And just to clarify what Trump calls “winning” as he visits Korea: The Korean trade deal (signed September 2018) has done nothing to reverse the bilateral US trade deficit (not that bilateral trade deficits matter, but it just shows its unclear what Trump was toasting in Korea as evidence he’s “winning”).

Just to be clear, the brilliantly negotiated, triumphant outcome for Trump is thus simply status quo that existed along before Trump started his bilateral trade wars (e.g: no tariffs and China buying US Ag products). Well, no, one thing is different: The US will provide China a shopping list of what it is supposed to buy from the US. Whoever came up with this unusual idea really distinguished himself/herself. Of course the Chinese will only buy what they need so they are humoring Trumps list — but what is the purpose of Trump going around threatening countries with forced shopping lists of US products? Is that how the Trump or the US wants to “win” the trade war?

{kind=link}