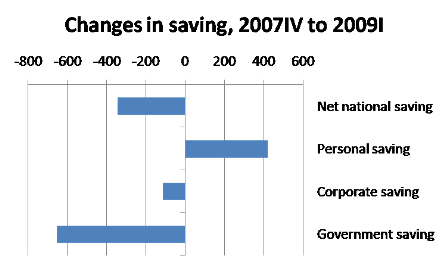

The sharp downturn in economic activity and world trade has caused many economists to frame analogies with the descending spiral of trade and protectionism in the 1930s. Under the WTO countries do have flexibility to impose safeguard restrictions, as well as duties to offset unfair trade practices. Reliance on these policies does seem to rise during economic declines, as shown by the following table presented by Roberta Roberta Piermartini of the WTO. Nevertheless, the existence of such flexibility may make countries more willing to accept greater liberalization in WTO negotiations.

Figure 1. Anti-dumping measures and business cycle

.png)

Read her discussion of these measures, and compare that analysis to the commentary by Chad Bown, who cautions against the long lives of such intervention. Also, consider the prescription for additional steps to avoid a downward spiral suggested by Simon J Evenett and Bernard Hoekman.

.jpg)

+(Small)+(2)+(WinCE).jpg)

{kind=link}

{kind=link}